Mobile payment solutions are convenient and fast. More and more customers have embraced the concept of using tablets and smartphones to pay for products and services. As the world is facing changes due to COVID-19, both traditional and eCommerce businesses need to quickly adapt to changing customer habits, including cashless payment methods via mobile devices. In this article, we’ll provide merchants with the latest trends in mobile payment so you can adapt your business to changing expectations in 2021.

What is mobile payment?

Mobile payments are regulated transactions made through mobile devices, including 2 main forms:

- Mobile wallet

- Mobile money transfer

In other words, mobile payment technology allows customers to make payments for goods and services digitally instead of with cash, credit cards, or checks.

Mobile payments global trends and market share

In some countries and certain markets, cash has gradually disappeared like the extinction of dinosaurs. Of course, there are still many reasons why some countries haven’t fully transitioned to mobile payment solutions. However, the mobile payment market certainly has a bright future.

- eMarketer predicts that 1.31 billion customers worldwide will be using a mobile payment app by 2023.

- IMARC forecasts that the global mobile payment market size will be more than $3 trillion by 2024.

- Mordor Intelligence indicates that payments by mobile will overtake credit cards and cash, and mobile payment global trends will increase by 26.93% from 2020 to 2025.

- Business Intelligence forecasts that the value of in-store mobile payments in the U.S. will be $128 billion by 2021.

- Mobile Payments World statistics show that the British are leading the trend of accepting mobile payment in Europe. 74% of the British population used mobile devices for financial management and digital purchases in 2016.

If retailers intend to compete and improve the customer experience, you should prepare for the growth of mobile payments trends from now. You should ensure that:

- Your stores accept mobile payment options.

- Your eCommerce websites have an optimized checkout process for mobile devices such as through Magento mobile app or a well-designed UX/UI with PWA storefront.

Types of mobile payments

By scope, there are 3 main types of mobile payment.

Proximity payment

- Offered by major companies such as Google, Samsung, and Apple

- Used as a POS payment method by participating merchants

Branded proximity payment

- Made through proximity technology such as Bluetooth technology, quick response (QR) codes, and near-field communication (NFC)

- Used within stores of big businesses such as Target or Walmart

Payment between individuals, or P2P payment

- Transferred between two individual credit cards or banking accounts through mobile app or website

- Used for any transactions like paying your rent, splitting a dinner bill between friends, or making an online bet such as with Venmo

Types of mobile payments

1. Point of sale (POS) solutions

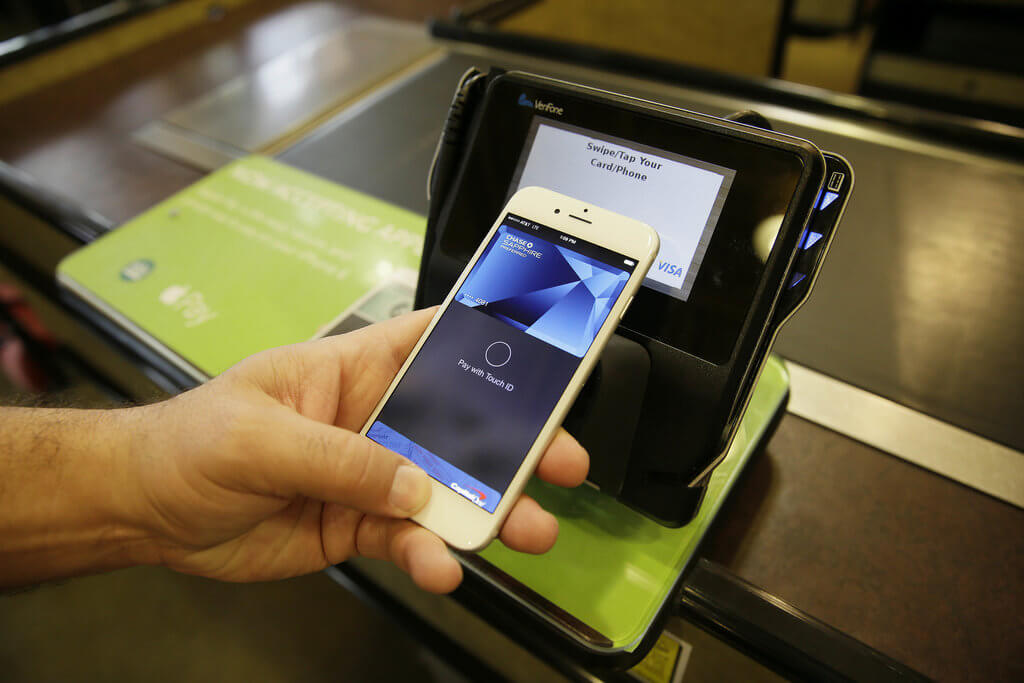

Near-field communication (NFC) payments

In business, near-field communication (NFC) transmits encrypted data to the POS devices in a direct and nearly instant manner. This saves a lot of time compared to PIN and chip technology.

- NFC in mobile devices uses close-proximity radio frequency identification to communicate with NFC-enabled card machines. In this way, customers don’t have to touch the POS to transfer information and the mobile devices just need to be near the terminal within a few inches.

- Digital wallets like Google Pay, Samsung Pay, and Apple Pay use NFC for contactless card machines.

- Many mobile providers are working to further develop this technology and increase its inherent security. For example, Apple Pay uses fingerprint recognition to complete payments by iPhone.

NFC payments are a rising mobile payment trend in many fields around the world.

- In London, you can tap the travel card to make NFC mobile payments for tube and bus stations.

- In China, NFC is accepted for payment on all public transport.

- In Japan, this mobile payment technology trend is being used to provide identity card information.

- In Nice, residents and visitors can use NFC to buy anything.

Sound wave-based payments

Sound wave-based (or audio signal-based) is the newer and more advanced mobile payment technology trend than NFC. It can work with most mobile devices.

- Instead of using existing technology such as banking apps or card terminals, mobile wallets, or NFC, sound wave-based payments transactions are processed via unique sound waves containing encrypted data about the payments. So, no internet is required.

- After the customer’s mobile device converts that data into an analog signal to complete the transaction, a wave is sent from the terminal to the mobile device to display payment details.

This method of mobile payments relies on more basic technology for payment processing:

- You can simply install the payment software and do not need any additional hardware.

- The solution is easy to deploy at a low cost, especially in countries and regions where residents can’t afford the most advanced smartphones.

Magnetic secure transmission (MST) payments

The final way to pay at POS terminals by mobile devices is through magnetic secure transmission (MST).

- This mobile payment trend allows mobile devices to emit a magnetic signal that mimics the magnetic stripe on a payer’s credit card. From there, the card terminal receives and processes it like a customer swiping a physical card through the machine.

- Most new terminals accept MST payments, while some older card readers may require a software update.

Samsung Pay uses both NFC and MST for contactless mobile payments. MST and NFC are both extremely secure because both use tokenization systems that are more secure than using a card.

2. Both in-store and remote payments

Mobile wallets

Mobile wallets, or digital wallets, use a variety of technologies in the payment process, the most common are QR codes and NFC.

- Mobile wallets typically store payment information in an application on a customer’s mobile device. It uses encrypted cards stored in your mobile wallet. In addition to debit and credit cards, you can add boarding passes, loyalty cards, and tickets.

- Digital wallets are very secure as it works through complex tokenization and encryption. Some use generated codes within time limits to process specific transactions.

With this mobile payment technology trend, Apple Pay allows users to touch the devices by their fingerprint to authenticate contactless payments for purchases on websites and in apps. Samsung Pay and Google Pay are also two other big players in mobile wallets.

Quick response (QR) code payments

You can now find quick responses (QR) in the most seemingly random places such as on product labels and in advertising. But you need to know that QR codes are also a mobile payment technology trend.

- QR works through certain banking apps where customers link their card to the apps of a merchant’s store.

- To scan the QR code, customers only need to point the camera to match fully the QR on the mobile screen.

QR code is considered as an alternative to entering card details because customers don’t have to type their unencrypted card details manually. It’s even more secure because customers’ card details are securely connected only after confirming they’re the rightful owner of the card.

- Currently, the majority of modern eCommerce businesses have adopted and accepted QR code payments on their websites.

- In the U.S., Walmart customers simply pay in-store by scanning a QR code in the Walmart Pay app.

>>> Might you like: Buckaroo POS by Magestore processes payments through QR codes.

3. Remote payments

Internet payments

Prior to 2010, internet payments were commonly referred to as wireless application protocol (WAP) payments. Now, internet payments refer to the situation when customers make payment over the internet (Wi-Fi or a 3G/4G network signal) using mobile apps or browsers like Chrome and Safari on mobile.

Customers can pay through the WAP application or a more limited-capacity browser, rather than a web browser with access to the entire internet.

- Customers enter their card details on the payment page directly on the website, or access the link and digital invoice attached in the email then redirect to pay on your website.

- After customers complete the payment, it will automatically charge a bank card tied to the mobile app, or their PayPal.

For now, internet payments are still one of the most popular mobile payment trends on smart mobile devices.

Payment links

Payment links, or ‘pay by link’ mobile payment technology refers to a link or a button that is sent via:

- Text messages

- Messaging apps

- Social media

- Emails

When the customer clicks the link, a payment page opens in the internet browser.

- Customers can enter their card details to process the transaction for a designated merchant.

- Customers either follow the amount of a preset value by the merchant or manually adjust the transaction total value.

- The merchant can then invoice to display the purchased product on the customer’s digital receipt.

SMS payments

SMS payments, or premium SMS, refer to making payment via a text message. Customers only need a prepaid SIM card or a phone contract and a phone with texting capabilities.

- Merchants send the customer a text message with payment information to their customer’s correct phone number.

- When the recipient accepts the payment amount, it will be added to their mobile bill.

In other words, customers pay through their phone network provider, which is pay-as-you-go or direct debit. Till now, SMS payments remain one of the most popular mobile payment trends for both donating to charity and paying for goods and services.

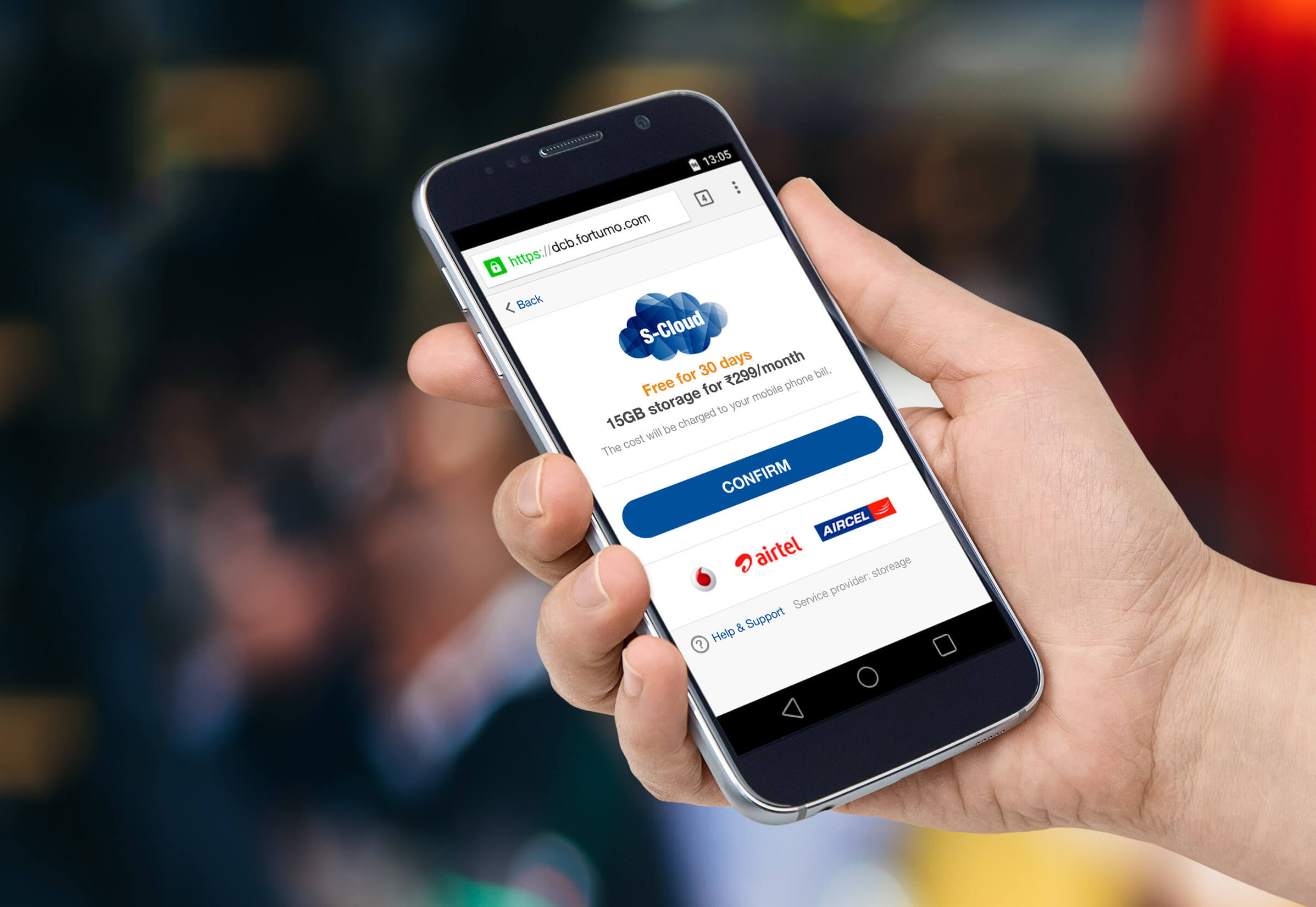

Direct carrier billing

Direct carrier billing (DCB) is customers paying the service providers directly through mobile service providers.

- Instead of using bank or card details, customers enter their phone number in an app or on a payment page.

- Customers need to go through some authentication steps to confirm they are the owner of the number like confirmation by text message.

- Payment will then be made from their prepaid SIM card or phone bill.

Digital services like the App Store and Google Play offer DCB payment options. This mobile payment technology trend is commonly used for digital subscriptions, charity donations, and TV voting.

Mobile banking

Mobile banking is an application developed by the bank.

- Customers can perform financial transactions directly from their bank accounts, such as making payments to others, paying bills, and peer-to-peer transfers.

- Common utilities of mobile payment technology trends are showing account balances, bank transfers, and transaction history.

Each bank will have its own way to verify you are the owner of the bank account on the app.

- Once customers have authenticated their account, the customer can use the phone number to log in and make a payment.

- Banks will set a separate limit of payment transactions through the app.

In some countries like the U.K. and Sweden, mobile banking has been very popular for paying bills or transferring money between individuals. Mobile banking is also very convenient to keep track of personal finances through banking apps.

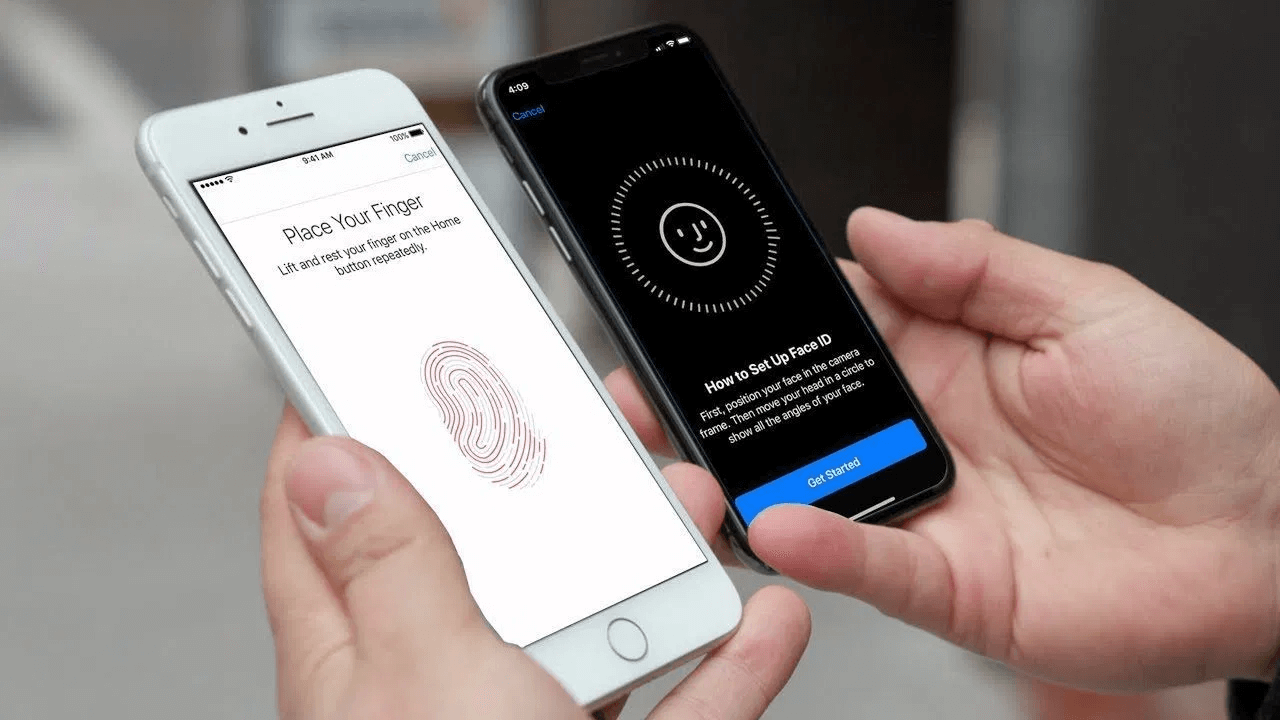

4. Biometric authentication

A future trend of mobile payment is using biometric authentication, instead of password or PIN, to authenticate the transaction. It’s famous for fast response, higher security, and widely application, including:

- Fingerprints

- Facial recognition

- Voice identification

Currently, there are many applications of biometrics in direct contactless payments like verification for mobile transactions. Research on mobile payments and data security forecasts that biometric authentication will increase by more than 1,000% by 2024, contributing more than $2.5 trillion in transaction volume. In 2019 alone, there were $228 billion in transactions for mobile payments using this technology.

5. Flexible payment options

Customers don’t only want the convenience of payment methods for mobile transactions, but also the flexibility of spending their budget. For this demand, merchants can offer buy now, pay later (BNPL) options for customers to check out. It’s now one of the most demanding mobile payments global trends.

- Once customers enter the credit card information, they can divide the total order value into smaller payments by time frames, such as a month, 6 months, or a year.

- Merchants tie the payment to the customer’s card, so you don’t need to use an intermediary application or additional credit checking.

In short, besides benefits to customers, merchants also can increase average order values and conversion rates when using flexible payment options.

Which mobile payment app is the best?

For contactless mobile payment technology trends, we recommend the top 5 mobile payment apps in 2021.

Apple Pay

Half of retails in the U.S. are accepting Apple Pay. We can name some popular businesses like Walgreens, Starbucks, Best Buy, and McDonald’s.

Pros

- No need to download app

- Work in iMessage and Macs

- Integrated with 2FA for higher security

Cons

- Only available on Apple devices

Google Pay

Many retail stores like Staples, Bloomingdale’s, Nike, KFC, and Chick-Fil-A, and online services such as DoorDash and Airbnb accept Google Pay.

Pros

- Preload on most Android devices

- Support from major card providers like American Express, Chase, Discover, and Citi

Cons

- Require Google Pay Send for person-to-person transaction

Samsung Pay

Most merchants like Samsung Pay because they do not need to opt-in to the program to accept the payments. Samsung Pay is compatible with all popular mobile payment technology trends, including NFC, EMV, and MST.

Pros

- Work with most regular credit card readers

- Be widely accepted by both merchants and customers

Cons

- Only available for Samsung mobile devices

PayPal

When it comes to mobile apps and online transactions, PayPal Pay has been around for a long time and offers seller protection when making online purchases.

Pros

- Provide ecosystem of accounts

- Transfer person-to-person without fee

Cons

- High service fees

Venmo

Venmo is very popular among millennials and useful for paying in online stores. However, quite a few retailers accept this mobile payment trend in physical stores, like Foot Locker or Forever 21.

Pros

- Charge no free for transactions without credit card

- Synchronize Facebook contacts

Cons

- Accepted by a limited number of merchants and retailers

Conclusion

Consumers are moving towards a world without physical cash, where mobile payments are the technology that will dominate the future. Mobile payment trends apparently encourage the growth of cashless transactions. Customers can use mobile payment applications, and digital payment options such as mobile wallets to pay at POS terminals and on eCommerce websites.

Major mobile technology providers are constantly finding new solutions to support the integration of mobile-friendly payment solutions. Retailers are reporting a huge increase in sales after they accept mobile payments. Needless to say, adapting to the future trends of mobile payment will ensure your store grows both online and offline in 2021.

Hats off to Magestore for their insightful exploration of mobile payment trends! This blog is a valuable compass navigating the ever-evolving landscape, providing businesses with strategic insights to stay ahead in the dynamic world of mobile transactions.

Great post!